WD-40 at a glance

WD-40 (WDFC) has drawn fresh attention after recent share price moves, with the stock closing at $238.53 and posting mixed short and longer term returns that may prompt investors to reassess expectations.

See our latest analysis for WD-40.

The sharp 5.7% 1 day share price pullback comes after a stronger run, with a 30 day share price return of 19.9% and a 3 year total shareholder return of 44.4%. This suggests longer term momentum remains intact despite recent volatility.

If this kind of move has you looking beyond household products, it could be a good time to scan the market for other ideas using our 22 top founder-led companies.

With WD-40 shares up 20.3% over 90 days and trading at $238.53, close to an analyst price target of $264.50, the key question is whether today’s valuation leaves upside on the table or if markets already price in future growth.

Most Popular Narrative: 9.8% Undervalued

With WD-40 closing at $238.53 against a most followed fair value estimate of $264.50, the current price sits below what that narrative implies.

The company's focus on premiumization of products, with targets for a compound annual growth rate for premium products exceeding 10%, is poised to improve net margins by shifting the product mix towards higher-margin offerings.

WD-40's strategy to divest its less profitable home care and cleaning brands is expected to position the company as a higher growth and higher gross margin enterprise, ultimately boosting operational margins and net margins once complete.

Want to see what is built into that $264.50 fair value? It rests on specific revenue growth assumptions, margin shifts, and a rich future earnings multiple. The full narrative lays out how those moving parts fit together.

Result: Fair Value of $264.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can change quickly if divestitures stall, or if foreign currency swings and higher operating costs squeeze the projected margins baked into that fair value.

Find out about the key risks to this WD-40 narrative.

Another View: Earnings Multiple Sends a Different Signal

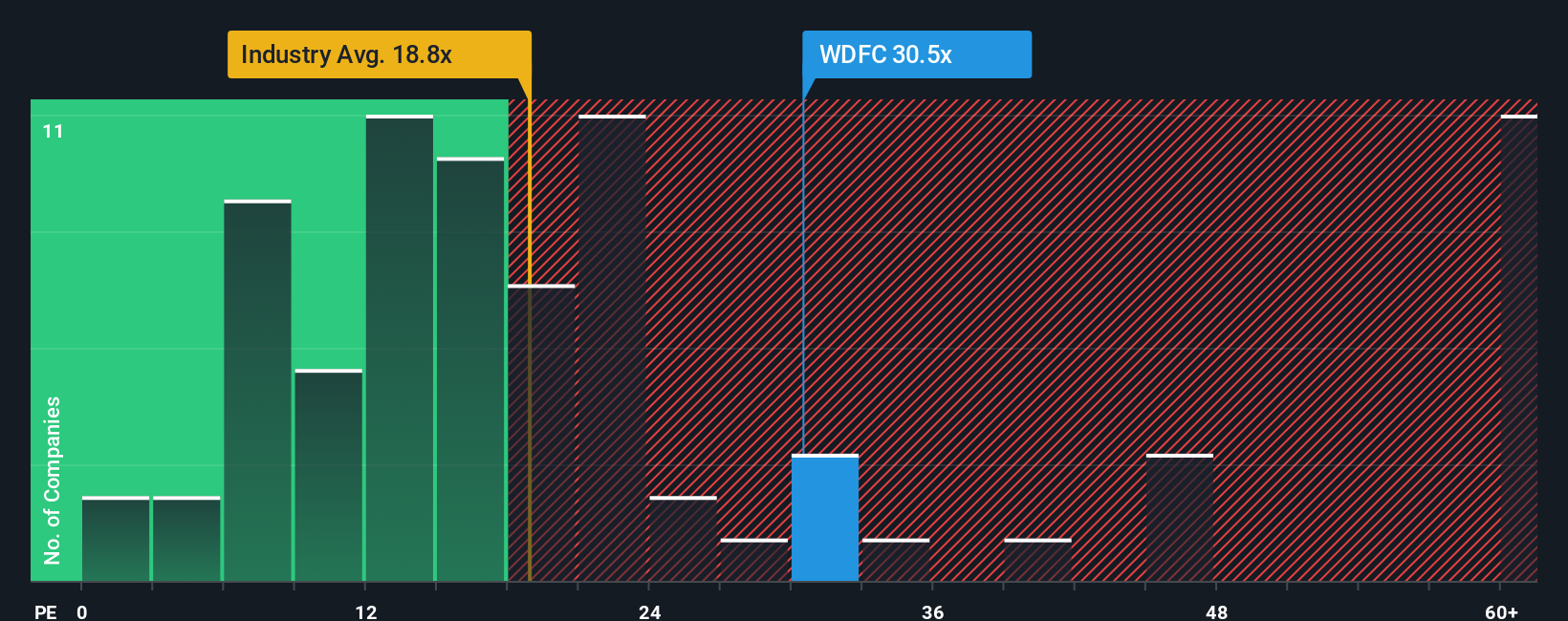

The narrative-based fair value of $264.50 points to WD-40 looking undervalued, but its current P/E of 36x tells a different story. That is far above the US Household Products peer average of 13.8x and a fair ratio of 14.2x, which suggests valuation risk if sentiment cools.

For a closer look at how that kind of gap between today’s P/E, peers, and the fair ratio can matter over time, See what the numbers say about this price — find out in our valuation breakdown. can help you unpack the numbers in more detail.

Build Your Own WD-40 Narrative

If parts of this story do not quite line up with your own view, or you would rather test the numbers yourself, you can build a customised narrative in just a few minutes by starting with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding WD-40.

Looking for more investment ideas?

If WD-40 has sharpened your thinking, do not stop here. Widen your watchlist now so you are not playing catch up later.

- Target long term compounding potential by scanning 53 high quality undervalued stocks that pair quality fundamentals with prices that sit below our fair value estimates.

- Strengthen your portfolio’s foundation by reviewing solid balance sheet and fundamentals stocks screener (45 results) that show robust financial positions and disciplined use of capital.

- Spot tomorrow’s potential standouts early with our screener containing 24 high quality undiscovered gems that highlight under followed companies with strong underlying metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com