Why Universal Technical Institute’s latest earnings matter for shareholders

Universal Technical Institute (UTI) released first quarter results that paired higher sales of US$220.84 million with lower net income of US$12.83 million, while also reaffirming full year 2026 revenue guidance of US$905 million to US$915 million.

See our latest analysis for Universal Technical Institute.

The earnings release and reaffirmed 2026 revenue guidance helped push Universal Technical Institute’s 1 day share price return to 6.9%. This built on a 22.18% year to date share price return at a last close of US$30.35. The 5 year total shareholder return of roughly 4x signals that the longer term payoff for holders has been very different to the recent 1 year total shareholder return of 6.9%.

If this earnings update has you thinking more broadly about where growth and risk might show up next, it could be worth scanning our 23 top founder-led companies as a starting list of ideas.

With UTI shares up strongly over 3 years and trading below the average analyst price target, yet showing lower recent net income, the real question is whether the current price understates future growth or already reflects it.

Most Popular Narrative: 19.3% Undervalued

Universal Technical Institute’s most followed narrative points to a fair value of $37.60 versus the last close of $30.35, which frames today’s move in a very different light.

The recently lifted growth restrictions on Concorde Career Colleges now allow for accelerated program launches and the addition of multiple new campuses a year ahead of plan, positioning the company for faster-than-anticipated revenue growth and increased market share starting as early as 2026.

Curious what has to happen for that valuation to stack up? The story quietly leans on brisk top line expansion, slimmer margins, and a richer future earnings multiple, all brought back to today using a specific discount rate.

The most popular narrative applies a discount rate of 7.23% to weigh those future cash flows against today’s $30.35 share price, and concludes that UTI is trading at a 19.3% discount to its $37.60 fair value estimate. Analysts in that narrative are building in rising revenue, changing profit margins and a higher P/E multiple several years out, then discounting those assumptions back to the present to arrive at the fair value figure.

Result: Fair Value of $37.60 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upbeat story can fray if aggressive campus expansion fails to fill seats, or if tighter regulation crimps access to funding and student demand.

Find out about the key risks to this Universal Technical Institute narrative.

Another View: What The Market Multiple Is Saying

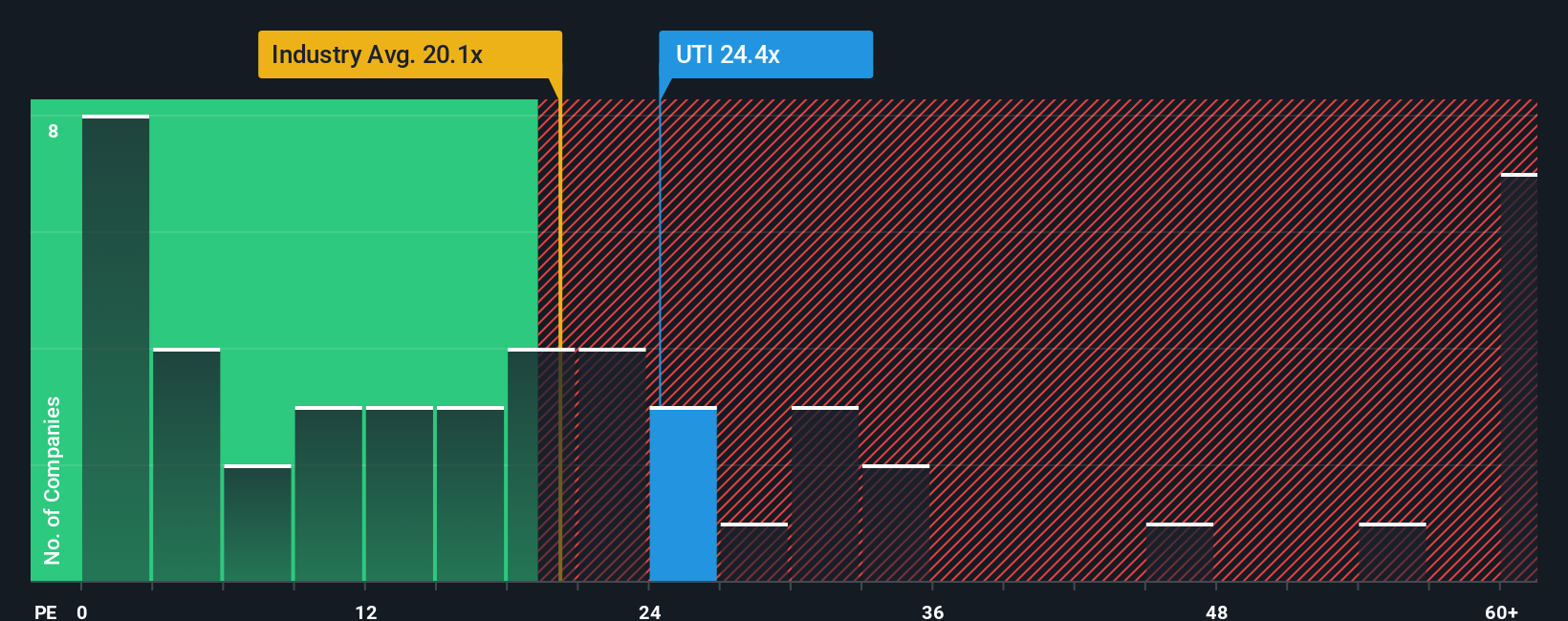

That 19.3% “undervalued” fair value sits awkwardly next to how UTI is actually priced today, with a P/E of 31.1x versus a peer average of 27.2x and a fair ratio of 18.3x. In plain terms, you are already paying a premium. Is the real risk that expectations are simply too high?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Universal Technical Institute Narrative

If you see the numbers differently or want to stress test your own assumptions, you can spin up a fresh Universal Technical Institute scenario in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Universal Technical Institute.

Looking for more investment ideas?

If UTI has sharpened your thinking, do not stop here. Broadening your watchlist with fresh ideas now could make a real difference to your next move.

- Spot opportunities in companies the market might be overlooking by checking our screener containing 23 high quality undiscovered gems and see which names stand out to you.

- Strengthen the quality of your watchlist with companies that carry less financial strain using our solid balance sheet and fundamentals stocks screener (45 results).

- Lock in income focused ideas by reviewing the 12 dividend fortresses and see which yields catch your attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com