Why the Synchrony renewal and guidance update matter for Polaris (PII)

Polaris (PII) is back in focus after Synchrony renewed their long running financing partnership, and management flagged an upcoming 2026 outlook update tied to the earlier than expected Indian Motorcycle separation.

For you as an investor, these two developments sit at the crossroads of how customers pay for vehicles and accessories, and how management now sees the company’s earnings power as its business mix shifts.

See our latest analysis for Polaris.

At a share price of $63.98, Polaris has seen a 2.83% 1 day share price gain after the Synchrony renewal and upcoming 2026 outlook update. Its 1 year total shareholder return of 43.18% contrasts with weaker 3 and 5 year total shareholder returns.

If this financing and guidance update has you thinking about where consumer and industrial demand could head next, it may be worth scanning 22 top founder-led companies as a way to spot other potential long term compounders.

With Polaris shares at $63.98, a 6% discount to the average analyst price target and a 43.18% 1 year total return, the key question is whether recent news leaves upside on the table or if the market already reflects future growth.

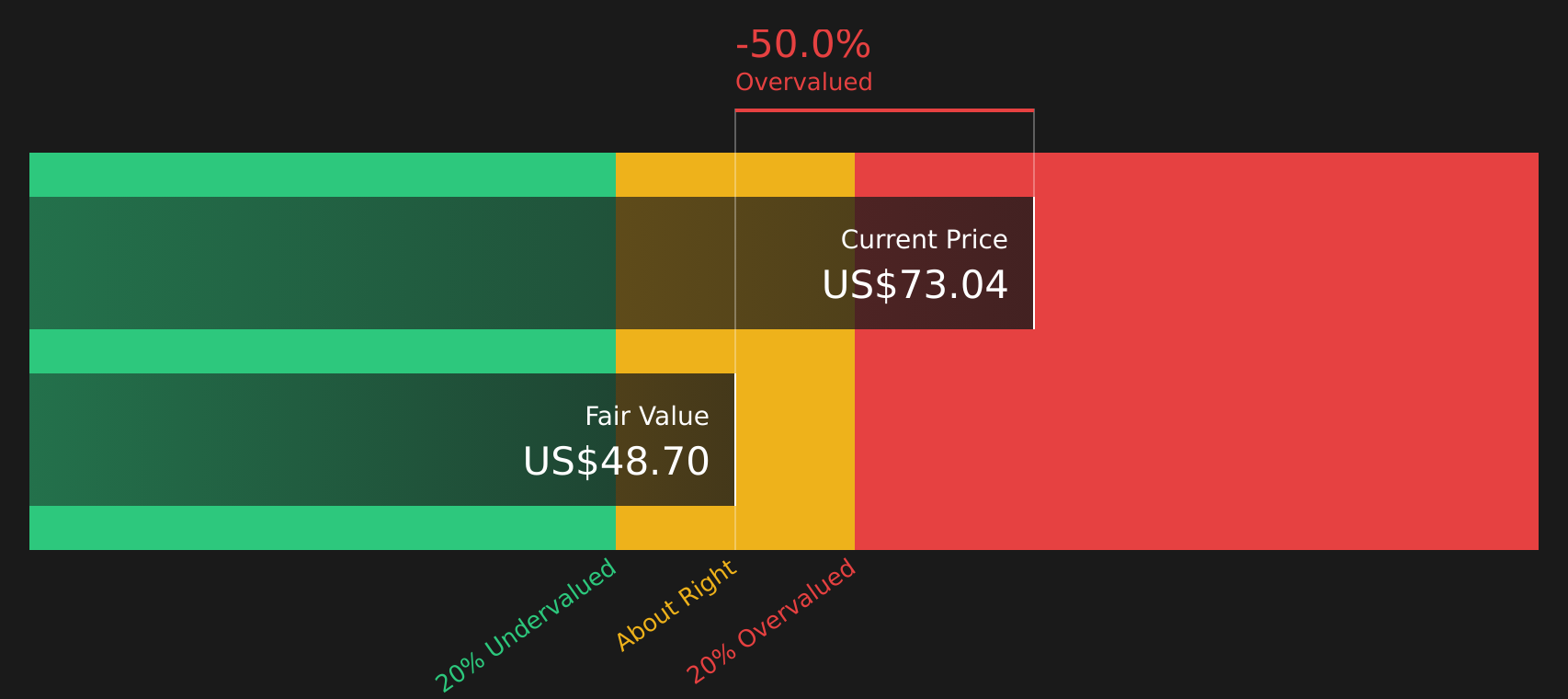

Most Popular Narrative: 5.7% Undervalued

With Polaris last closing at $63.98 against a widely followed fair value of $67.85, the leading narrative sees modest upside supported by earnings power and margin potential under an 8.10% discount rate.

Polaris is executing on new product launches and innovations, such as the digital helm in their boating lineup, which are expected to enhance their portfolio and drive future sales growth, potentially increasing revenue.

Polaris has mobilized a tariff mitigation strategy to offset expected $320 million to $370 million gross tariff costs, which aims to reduce the financial impact and improve earnings by maintaining operational efficiencies and preserving liquidity.

Want to see what really sits behind that fair value gap? The narrative leans on a mix of steady top line assumptions, rebuilding profit margins and a future earnings multiple that may surprise you. The full set of forecasts joins these pieces into a single valuation story.

Result: Fair Value of $67.85 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh risks such as higher tariff costs pressuring margins and any renewed softness in powersports demand that could challenge these assumptions.

Find out about the key risks to this Polaris narrative.

Another View: DCF Paints A Harsher Picture

While the narrative fair value of $67.85 frames Polaris as 5.7% undervalued, our DCF model points the other way, with an estimated future cash flow value of $13.67. That gap suggests a wide range of possible outcomes. Which story do you think is closer to reality?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Polaris for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

After all this, are you feeling cautious or curious about where Polaris really stands, and ready to act on your own view using 2 key rewards and 3 important warning signs?

Ready to hunt for your next idea?

If Polaris has sharpened your focus, do not stop here. Use the Simply Wall St screener to quickly spot other opportunities that could suit your portfolio.

- Target higher quality at attractive prices by scanning our 51 high quality undervalued stocks that combine solid fundamentals with potentially appealing valuations.

- Prioritise sleep at night stability with 78 resilient stocks with low risk scores that score well on resilience and risk factors.

- Get ahead of the crowd by checking the screener containing 23 high quality undiscovered gems that our filters surface before they hit more radars.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com