- On 23 February 2026, US Foods Holding Corp. launched Menu IQ, an AI-powered menu profitability tool integrated into its MOXe platform, offering customers recipe cost calculations, real-time margin tracking, and optimization insights at no additional cost.

- This move deepens US Foods’ role as a technology partner to foodservice operators, embedding data-driven menu management directly into its existing digital ecosystem.

- Next, we’ll examine how embedding AI-driven menu profitability tools into MOXe could influence US Foods’ longer-term investment narrative.

This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

US Foods Holding Investment Narrative Recap

To own US Foods, you need to believe it can keep converting a low margin distribution model into steadier earnings through digital tools, private label penetration, and disciplined capital allocation, while managing its reliance on “food away from home” demand. The launch of Menu IQ looks directionally supportive for near term execution on digital efficiency, but it does not materially change the immediate risk that softer case volume could still weigh on revenue growth if industry demand stays weak.

Among recent announcements, the ongoing US$1,000 million share buyback authorization stands out in this context, as it reinforces a capital return program that sits alongside US Foods’ investment in tools like MOXe and Menu IQ. For investors, the pairing of heavy technology spend with sizeable repurchases can be appealing if earnings keep pacing ahead of costs, but it may also magnify concerns about leverage and financial flexibility if industry conditions were to worsen.

Yet behind these digital gains, investors still need to watch the risk that softer “food away from home” spending could...

Read the full narrative on US Foods Holding (it's free!)

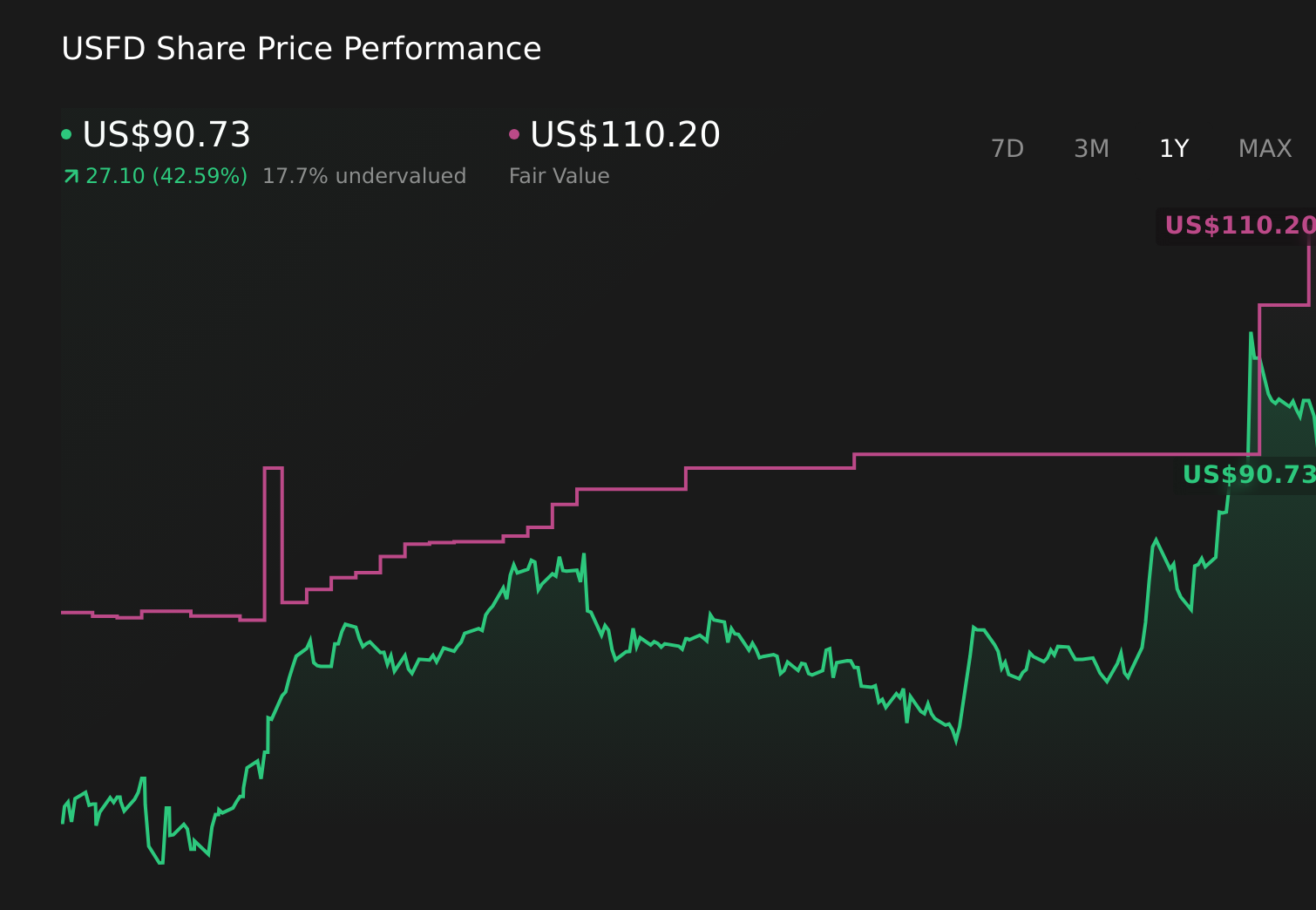

US Foods Holding's narrative projects $45.1 billion revenue and $1.1 billion earnings by 2028. This requires 5.3% yearly revenue growth and a roughly $0.5 billion earnings increase from $553.0 million today.

Uncover how US Foods Holding's forecasts yield a $110.20 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Seven fair value estimates from the Simply Wall St Community span roughly US$78.52 to US$154.77, underscoring how far apart individual views on US Foods can sit. When you set those against the company’s push into tools like MOXe and Menu IQ to improve profitability, it becomes clear you should compare multiple perspectives before deciding how much of the growth and margin story you want to underwrite.

Explore 7 other fair value estimates on US Foods Holding - why the stock might be worth as much as 60% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your US Foods Holding research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free US Foods Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate US Foods Holding's overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 33 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com