- Walker & Dunlop, Inc. recently hired Mark Washington as managing director of Capital Markets, Multifamily Investment Sales, to lead its entry into Pacific Northwest multifamily investment sales from a new base in Seattle.

- By adding an institutional broker involved in over US$50.00 billion of capital markets transactions, Walker & Dunlop is deepening its access to one of the country’s most actively traded multifamily regions.

- Next, we’ll examine how this expansion into Pacific Northwest multifamily investment sales could influence Walker & Dunlop’s housing-focused investment narrative.

Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

Walker & Dunlop Investment Narrative Recap

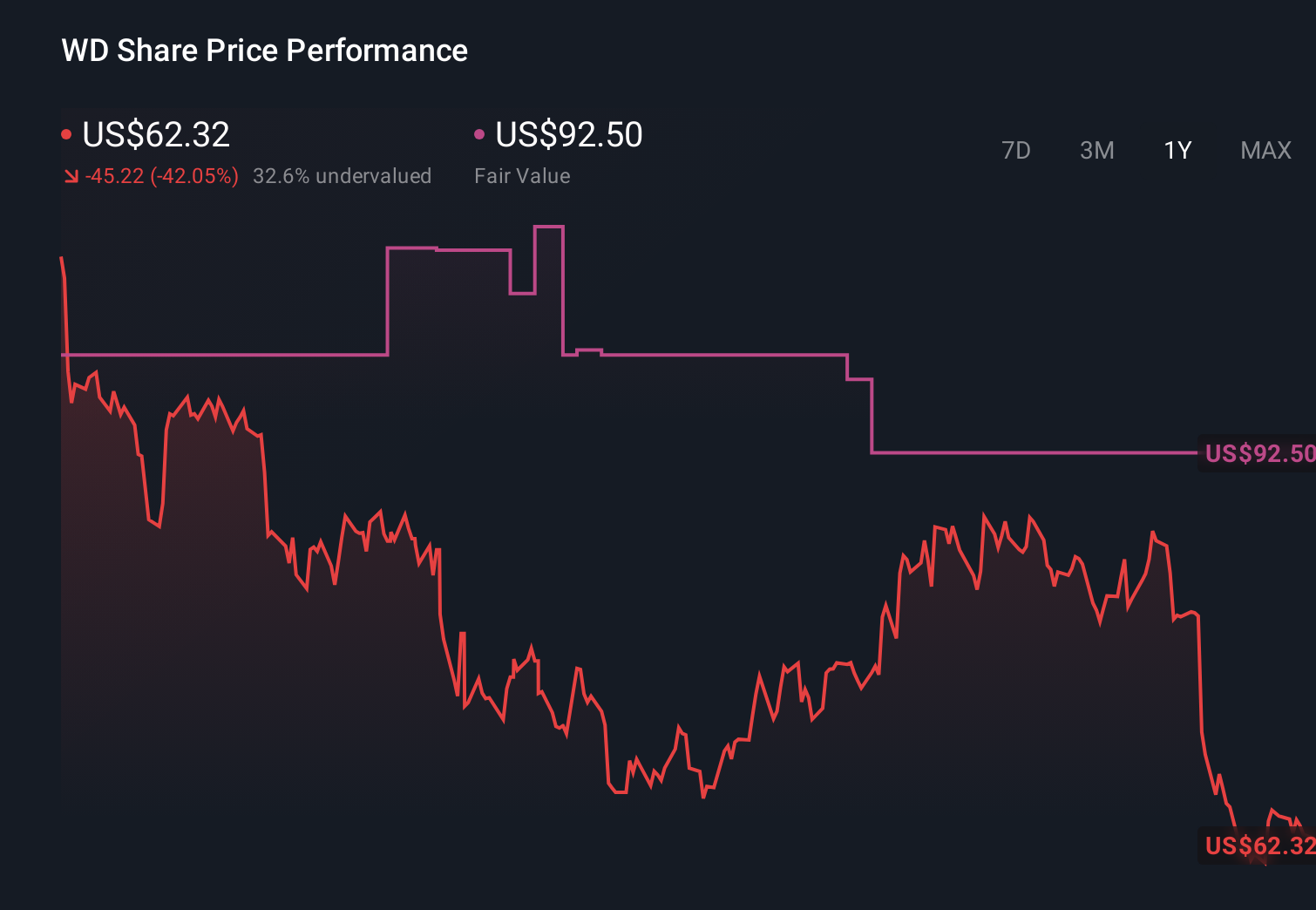

To own Walker & Dunlop, you need to believe in a long term housing and multifamily financing story, supported by both origination and fee-based servicing. The Seattle hire strengthens the multifamily investment sales push in a key region, but does not fundamentally change the near term picture, where the main catalyst is a recovery in transaction volumes and the biggest risk remains pressure on profitability after the recent swing to a quarterly net loss.

The most relevant recent announcement is the fourth quarter and full year 2025 result, where revenue grew year on year but earnings fell and Q4 turned to a loss. Against that backdrop, expanding into Pacific Northwest multifamily investment sales with an experienced institutional broker fits with the effort to deepen fee income, yet it also highlights how dependent overall performance still is on broader commercial real estate volumes and margins.

Yet behind the appeal of multifamily growth, investors should be aware of how sensitive Walker & Dunlop remains to...

Read the full narrative on Walker & Dunlop (it's free!)

Walker & Dunlop's narrative projects $1.5 billion revenue and $233.2 million earnings by 2028. This requires 11.2% yearly revenue growth and a $125.4 million earnings increase from $107.8 million today.

Uncover how Walker & Dunlop's forecasts yield a $65.00 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community put fair value for Walker & Dunlop between US$32.93 and US$65, reflecting very different expectations. When you set those views against the risk that high or volatile interest rates can suppress commercial real estate transaction and refinancing activity, it becomes even more important to compare several independent takes on the company’s prospects.

Explore 3 other fair value estimates on Walker & Dunlop - why the stock might be worth as much as 29% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Walker & Dunlop research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Walker & Dunlop research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Walker & Dunlop's overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 29 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com