Recent interest in Pool (POOL) has picked up after the company reaffirmed its capital return approach. The Board declared a quarterly cash dividend of $1.25 per share payable on March 26, 2026.

See our latest analysis for Pool.

The reaffirmed dividend comes after a tough share price stretch, with Pool’s 1 month share price return at a 16.3% decline and 1 year total shareholder return down 39.2%. This suggests sentiment has cooled even as management keeps emphasizing consistent cash returns.

If this pullback has you thinking about where else steady cash generators might emerge, it could be a good time to scan our list of 20 top founder-led companies and see what stands out.

So with the share price under pressure, a value score of 4, and the stock trading below one intrinsic value estimate, is Pool quietly offering a reset entry point, or is the market already baking in its cash generation profile?

Most Popular Narrative: 17.4% Undervalued

Pool's latest close at $217.92 sits well below the narrative fair value of $263.70, putting the focus squarely on the cash flow story behind that gap.

The analysts have a consensus price target of $333.273 for Pool based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $375.0, and the most bearish reporting a price target of just $285.0.

Want to see what sits between today's price and that higher fair value? The narrative leans on steady revenue progress, firmer margins, and a richer future earnings multiple.

Result: Fair Value of $263.70 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, softer recent earnings and pressure on new pool construction could still challenge the idea that recurring maintenance alone supports the current undervaluation story.

Find out about the key risks to this Pool narrative.

Another Take On Value

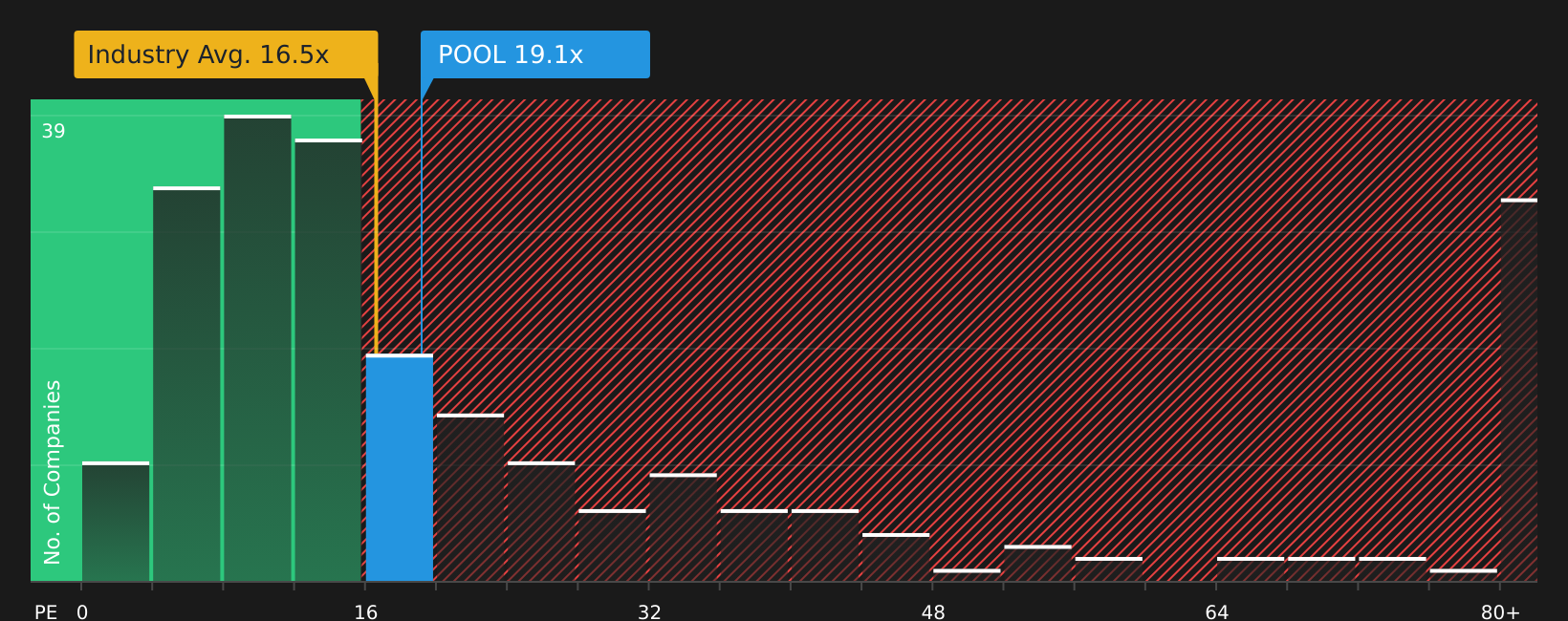

While the narrative fair value suggests Pool is undervalued, the P/E picture sends a cooler message. At 19.8x earnings, Pool trades above the global Retail Distributors average of 15.1x and above its own fair ratio of 15x, which points to valuation risk if sentiment sours further.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Does this mix of pressure and potential leave you uncertain? Act while the facts are fresh and weigh both sides by checking the 4 key rewards and 1 important warning sign for yourself.

Looking for more investment ideas?

If Pool has you rethinking your watchlist, this is the moment to widen your lens and hunt for other opportunities that better fit your goals.

- Start by targeting quality at a discount and see which companies our 47 high quality undervalued stocks highlight for potential mispriced strength.

- Prioritise resilience and scan the 73 resilient stocks with low risk scores to focus on businesses with steadier risk profiles that may suit a calmer ride.

- Hunt for future standouts before they are crowded by checking our screener containing 24 high quality undiscovered gems and spotting ideas others might be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com