Recent share performance and what it might signal

V.F (VFC) has been under pressure recently, with the stock showing a 5.1% decline over the past day, 10.8% over the past week, and 18.2% over the past month. This may prompt investors to reassess expectations.

See our latest analysis for V.F.

At a share price of US$17.32, V.F’s recent weakness extends beyond the latest drop. A 30 day share price return of negative 18.2% has contributed to a 5 year total shareholder return of negative 74.25%, which suggests momentum has been fading rather than building.

If this pullback has you thinking about where else to put fresh capital to work, it could be a good moment to look at our list of 20 top founder-led companies as a way to uncover other potential long term compounders.

With V.F shares sitting at US$17.32 and trading at what some models suggest is a 27.27% discount to intrinsic value, you have to ask: is this a genuine reset for a long established apparel group, or is the market already looking through to future growth?

Most Popular Narrative: 2.2% Overvalued

With V.F shares at $17.32 versus a widely followed fair value estimate around $16.95, the current price sits slightly above that narrative anchor and puts the focus firmly on how much earnings power can really be pulled from the core brands.

The strategic focus on expanding higher-margin channels, including direct-to-consumer and e-commerce, is beginning to drive improved gross margins and deeper customer engagement, which is expected to lift both revenue growth and net margins over time as V.F. capitalizes on the sustained consumer shift toward digital and premium shopping experiences.

Curious what has to happen behind the scenes for that fair value to make sense? The narrative leans on faster earnings growth than sales, a higher long term margin profile, and a future profit multiple that needs the Vans recovery story to eventually cooperate. The interesting part is how those moving pieces fit together to justify only a small gap between fair value and today’s price.

Result: Fair Value of $16.95 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still pressure points, including prolonged Vans weakness and elevated leverage above 4x, that could easily derail the margin and earnings narrative.

Find out about the key risks to this V.F narrative.

Another angle from the SWS DCF model

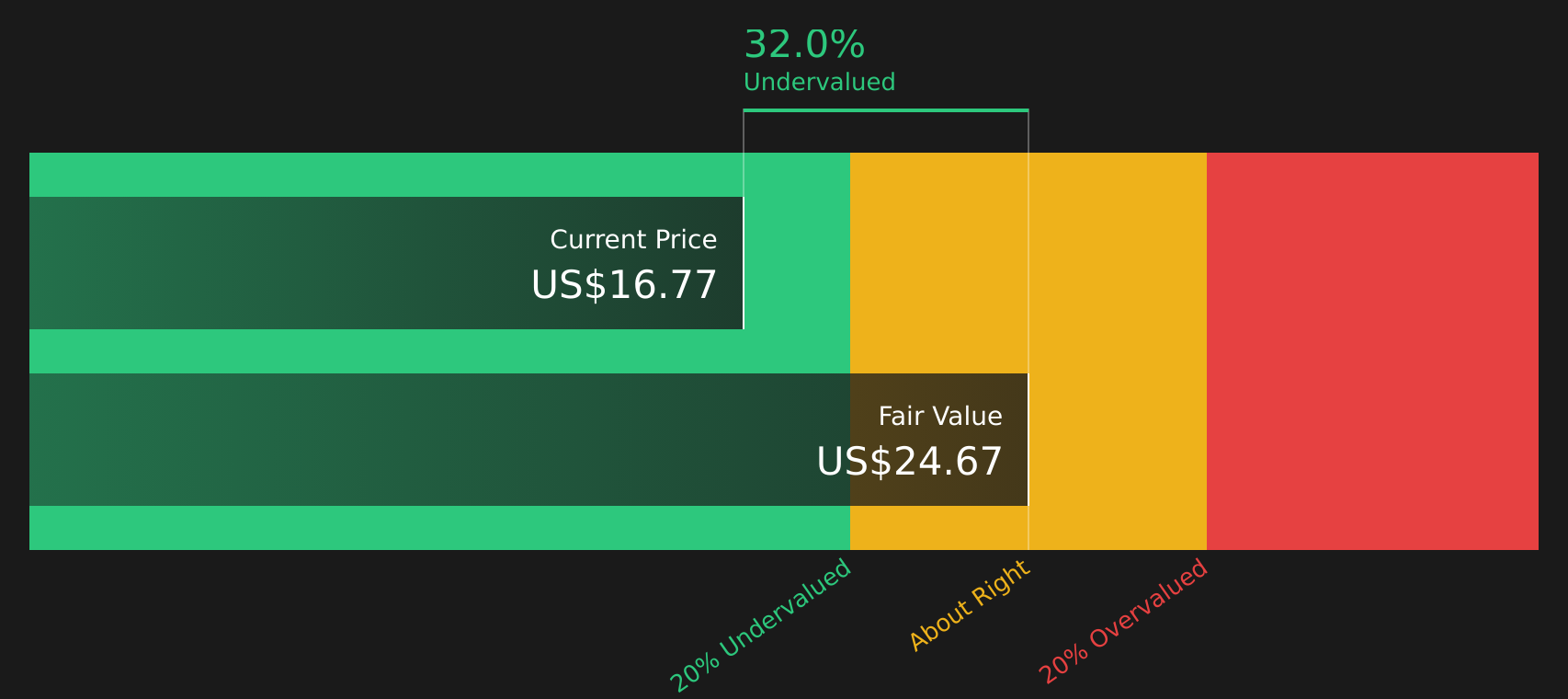

While the narrative-based fair value sits at $16.95 and points to V.F as slightly overvalued at $17.32, our DCF model paints a different picture. On that view, the shares are trading about 27.3% below an estimated future cash flow value of $23.81, which raises a simple question for you: is the story too cautious, or is the cash flow model too generous?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out V.F for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals from the story so far? If you want a clearer view, move quickly and weigh the tension between the 3 key rewards and 3 important warning signs yourself.

Looking for more investment ideas?

If you are on the fence about V.F, do not sit still. Use this moment to scan fresh ideas that could better match your goals and risk comfort.

- Spot potential value opportunities early by checking out our list of 50 high quality undervalued stocks that currently screen as attractively priced with solid fundamentals.

- Strengthen the income side of your portfolio by reviewing 16 dividend fortresses, focused on companies offering yield with an emphasis on resilience.

- Prioritise stability and capital protection by assessing 63 resilient stocks with low risk scores, where the focus is on businesses with more measured risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com