- In February 2026, Marqeta, Inc. reported fourth-quarter 2025 sales of US$172.11 million with sharply reduced net losses, issued 2026 guidance calling for double-digit net revenue and gross profit growth, and filed a US$106.08 million shelf registration for 25,935,338 Class A shares tied to an employee stock plan.

- This combination of improving financial results, clearer growth expectations, and a sizeable employee share offering highlights how Marqeta is balancing expansion with capital and workforce incentives.

- Now we’ll consider how Marqeta’s double-digit 2026 growth guidance might reshape the existing investment narrative for the business.

Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

Marqeta Investment Narrative Recap

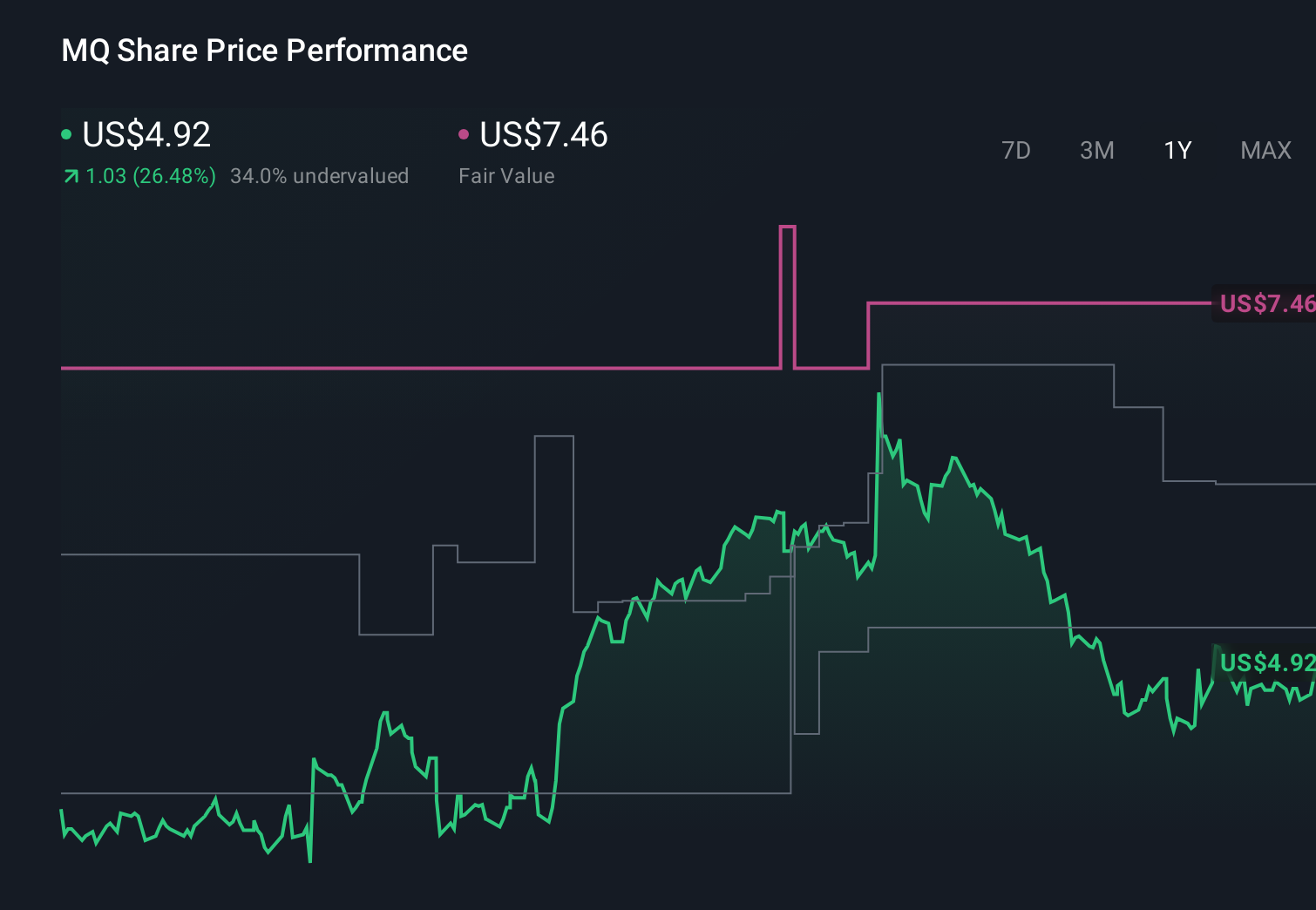

To own Marqeta, you need to believe that its card-issuing platform can keep riding digital payments and embedded finance adoption, while gradually improving profitability. The latest results and 2026 guidance reinforce that the near term catalyst is execution on revenue and gross profit growth, but customer concentration and industry competition still look like the biggest risks. The new shelf registration and share issuance tied to employees do not materially change those near term drivers.

The most relevant update here is Marqeta’s 2026 outlook, calling for net revenue growth of 12% to 14% and gross profit growth of 10% to 12%. That guidance frames how much upside the business might capture from digital payments and embedded finance, and how quickly it can move toward sustained profitability, while investors continue to weigh concentration, regulatory, and competitive pressures against that growth profile.

But investors also need to be aware that customer concentration risk could still hurt faster than the new growth guidance might help...

Read the full narrative on Marqeta (it's free!)

Marqeta's narrative projects $900.6 million revenue and $47.9 million earnings by 2028.

Uncover how Marqeta's forecasts yield a $5.73 fair value, a 42% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue could reach about US$1.0 billion and earnings around US$195 million by 2028, so compared with the consensus narrative and today’s 2026 growth guidance, you can see how views on Marqeta’s potential are spread wide and may shift again as new results come through.

Explore 4 other fair value estimates on Marqeta - why the stock might be worth 8% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Marqeta research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free Marqeta research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Marqeta's overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 16 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 29 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com