- Polaris recently gained attention as Wells Fargo began covering the stock with an Equal-Weight rating, while the company also confirmed plans to sell its Indian motorcycle brand to Carolwood in the first quarter of 2026.

- Together with Polaris’s inclusion in the Russell 1000 ETF, these moves highlight a shift toward refocusing its portfolio and potentially broadening its investor base.

- Next, we’ll explore how Polaris’s planned divestiture of the Indian motorcycle brand could influence the company’s existing investment narrative.

Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

Polaris Investment Narrative Recap

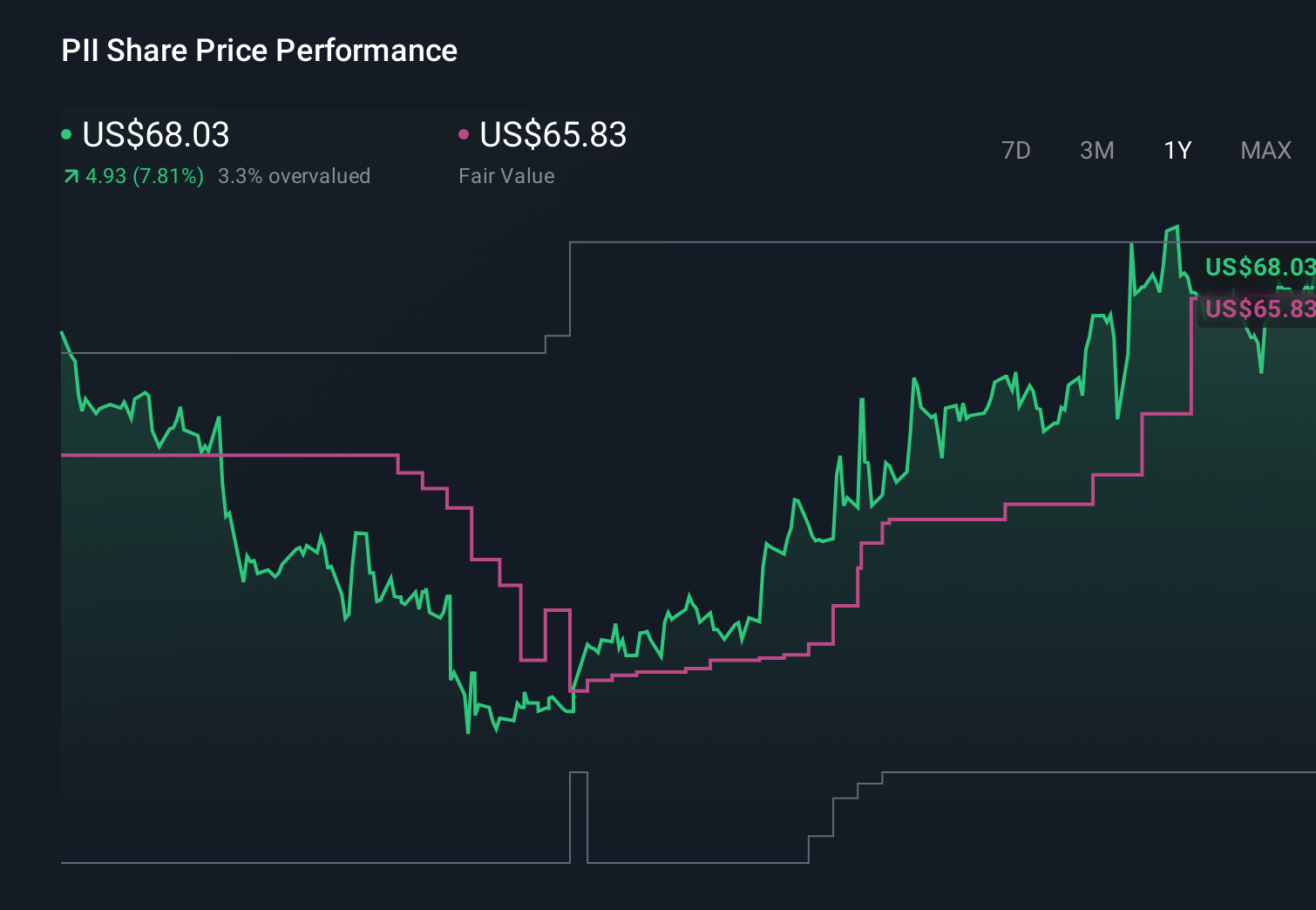

To own Polaris today, you need to believe its powersports and utility platform can translate new products and cost control into a return to profitability, despite recent losses and tariff uncertainty. The Indian motorcycle sale and Russell 1000 ETF inclusion do not materially change the near term earnings overhang or tariff risk, but they could help simplify the story and support liquidity if execution on core off road and marine products holds up.

Among the recent developments, the planned divestiture of the Indian motorcycle brand to Carolwood in early 2026 is most directly tied to Polaris’s current reset. It comes as the company is unprofitable, facing high tariff related cost pressure and choppy demand, while still rolling out premium offerings like the RANGER and XPEDITION lines that underpin the main earnings catalyst: a cleaner, more focused powersports portfolio.

But against those potential benefits, investors should be aware that tariff costs and a still weak international business could...

Read the full narrative on Polaris (it's free!)

Polaris' narrative projects $7.5 billion revenue and $224.6 million earnings by 2028.

Uncover how Polaris' forecasts yield a $67.85 fair value, a 32% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a far harsher picture, assuming roughly flat revenue near US$7.1 billion and only US$219.8 million in earnings by 2028, which contrasts sharply with the more optimistic views you have seen so far and may look very different once the Indian divestiture and other recent news are fully reflected.

Explore 4 other fair value estimates on Polaris - why the stock might be worth 37% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Polaris research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Polaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polaris' overall financial health at a glance.

Seeking Other Investments?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com