Why Pool stock is drawing attention now

Pool (POOL) has been catching investor interest after a stretch of weak share performance, including negative returns over the past month and past 3 months, set against a backdrop of ongoing revenue and net income growth.

See our latest analysis for Pool.

Pool’s recent 1 day share price return of 1.23% follows a 30 day share price decline of 22.27% and a 1 year total shareholder return decline of 35.66%, which suggests that momentum may still be weakening rather than shifting decisively higher.

If this pullback has you looking beyond Pool, it could be a good moment to widen your watchlist with 19 top founder-led companies as fresh ideas for your next stock search.

So with Pool trading at a discount to some valuation estimates despite ongoing revenue and net income growth, is this slump setting up a potential entry point or is the market already correctly pricing in its future trajectory?

Most Popular Narrative: 22.3% Undervalued

Pool’s most followed narrative sees fair value at $266.09 versus the last close of $206.64, framing today’s share price as meaningfully below that estimate while leaning on modest growth and stable margins.

The aging installed U.S. pool base continues to create steady, nondiscretionary demand for renovation, maintenance, and parts, partially insulating revenues from new build cyclicality and underpinning durable long-term earnings growth.

Curious how steady maintenance demand, measured revenue growth, and margin assumptions combine into that fair value number? The full narrative lays out a precise earnings path, share count expectations, and the valuation multiple required to support that price.

Result: Fair Value of $266.09 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent housing and discretionary spending headwinds, along with inflation and margin pressure, could still challenge earnings stability and weaken confidence in that undervalued narrative.

Find out about the key risks to this Pool narrative.

Another View: Earnings Multiple Sends A Different Signal

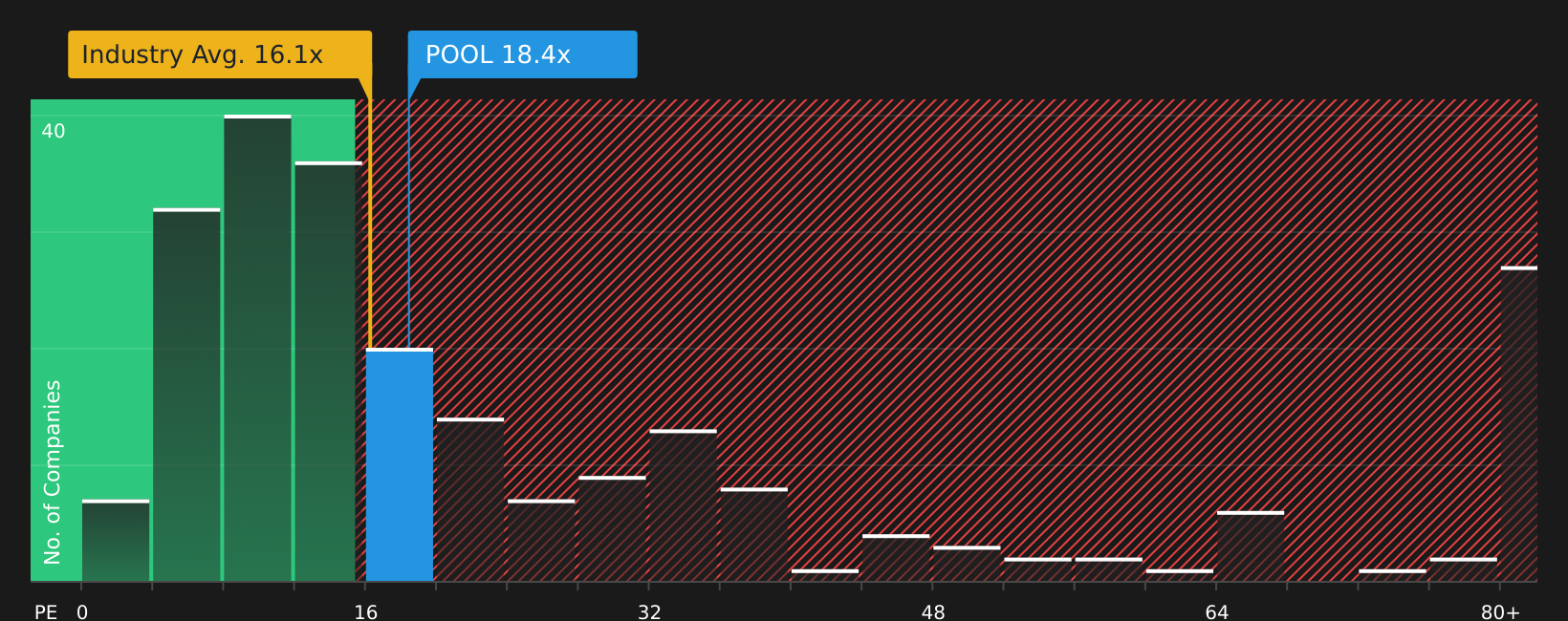

While the narrative and our fair value estimate of $266.09 point to Pool trading at a 35.6% discount, the earnings multiple tells a more cautious story. The current P/E of 18.8x is higher than both the global Retail Distributors average of 15.4x and our fair ratio of 14.9x, which suggests some valuation risk if sentiment or earnings soften further.

That premium is partly tempered by Pool trading below peers that sit around 36.6x, but you are still paying more than both the wider industry and the level our fair ratio suggests the market could move toward. The question is whether recurring revenue and forecast 4.6% annual earnings growth justify staying above that 14.9x anchor.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment mixed and the data pulling in both directions, now is a good time to look through the numbers yourself and decide where you stand, starting with 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Pool has your attention, do not stop there. Broaden your watchlist now so you are not the one hearing about the next opportunity after it moves.

- Target value by scanning 48 high quality undervalued stocks that pair compressed prices with solid fundamentals and see which names deserve a closer look.

- Prioritise resilience with 68 resilient stocks with low risk scores and focus on companies where risk indicators stay contained instead of leaving you guessing.

- Spot underfollowed stories using our screener containing 26 high quality undiscovered gems and get familiar with quality businesses before they are crowded trades.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com