- Earlier in March 2026, Paychex, Inc. was again named one of the World’s Most Ethical Companies by Ethisphere, while analysts suggested its fiscal Q3 results could outperform conservative guidance thanks to seasonal tax-form fees and additional client funds held during bonus season.

- This combination of recognized ethical standards and potentially better-than-expected operational performance highlights how corporate culture and seasonal revenue drivers may be influencing investor confidence in Paychex.

- Next, we’ll examine how the prospect of Q3 outperformance and renewed ethics recognition affects Paychex’s existing AI-focused investment narrative.

Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

Paychex Investment Narrative Recap

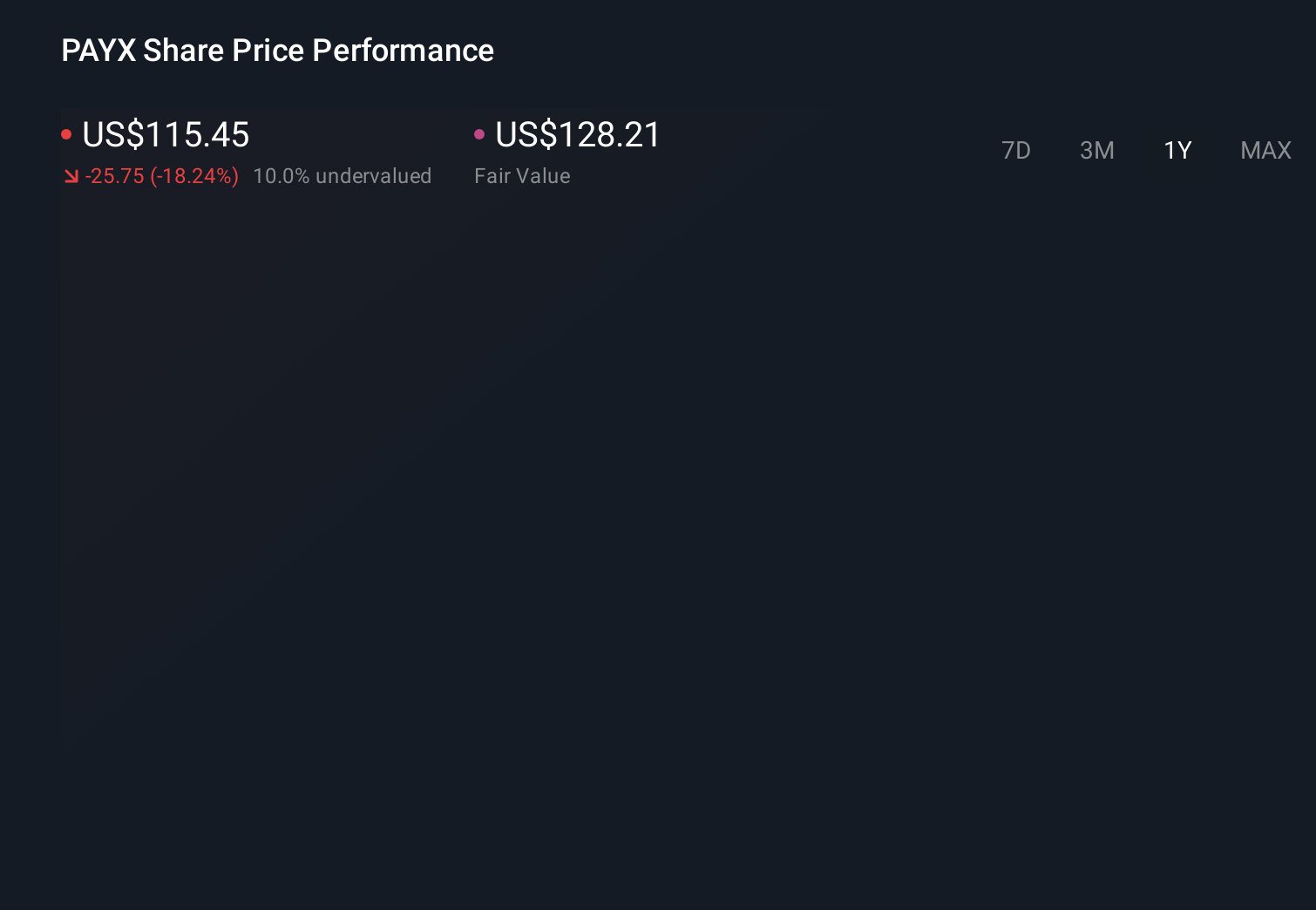

To own Paychex, you generally have to believe its payroll and HR platforms can stay essential for small and midsize businesses, even as AI reshapes the industry and integration of Paycor adds complexity. In the near term, the key catalyst is fiscal Q3 results on March 25, where seasonal tax-form fees and bonus float could matter more to sentiment than the latest ethics award. The biggest current risk remains pricing pressure and softer client behavior, which this news does not materially change.

The recent recognition by Ethisphere as one of the World’s Most Ethical Companies for the 18th time is most relevant here, because it reinforces Paychex’s culture and governance story just as it leans harder into AI tools and the Paycor integration. For some investors, a long ethics track record can make heavy tech investment and M&A complexity easier to underwrite when weighing upcoming AI-related product launches and Q3 guidance against ongoing macro and pricing headwinds.

Yet behind the ethics accolades, there is a quieter pricing and client behavior risk that investors should be aware of...

Read the full narrative on Paychex (it's free!)

Paychex's narrative projects $7.5 billion revenue and $2.3 billion earnings by 2028. This requires 10.2% yearly revenue growth and about a $0.6 billion earnings increase from $1.7 billion today.

Uncover how Paychex's forecasts yield a $116.93 fair value, a 26% upside to its current price.

Exploring Other Perspectives

While consensus focuses on seasonal Q3 upside, the most optimistic analysts were already assuming revenue could reach about US$7.8 billion and earnings US$2.5 billion by 2029, which is far more upbeat than concerns about smaller deal sizes and weaker insurance volumes might suggest, so you should recognize how far opinions can differ and consider how this new ethics and Q3 narrative might shift those expectations.

Explore 5 other fair value estimates on Paychex - why the stock might be worth as much as 71% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Paychex research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Paychex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Paychex's overall financial health at a glance.

Want Some Alternatives?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Find 53 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com