If you are wondering whether FedEx is still attractively priced after a strong run, this article walks through what the current share price may be implying and how that stacks up against different valuation yardsticks.

FedEx closed at US$355.78, with returns of 1.0% over the last week, an 8.4% decline over the last 30 days, 21.4% year to date, 50.1% over 1 year, 72.4% over 3 years, and 40.5% over 5 years. These figures provide a sense of how expectations and risk perceptions have shifted over different time frames.

Recent news flow around FedEx has centered on its role as a major global logistics player and its exposure to global trade and parcel volumes. This tends to keep the stock in focus when investors assess economic activity and supply chain trends. That context helps explain why the share price can be sensitive to changes in sentiment about shipping demand, e commerce activity, and efficiency efforts in the delivery network.

On Simply Wall St's valuation checks, FedEx has a value score of 4 out of 6, which suggests some valuation metrics still point to potential mispricing, while others are more balanced. The next sections will walk through those methods in more detail before finishing with a broader way to think about what the valuation really means for you as an investor.

Approach 1: FedEx Discounted Cash Flow (DCF) Analysis

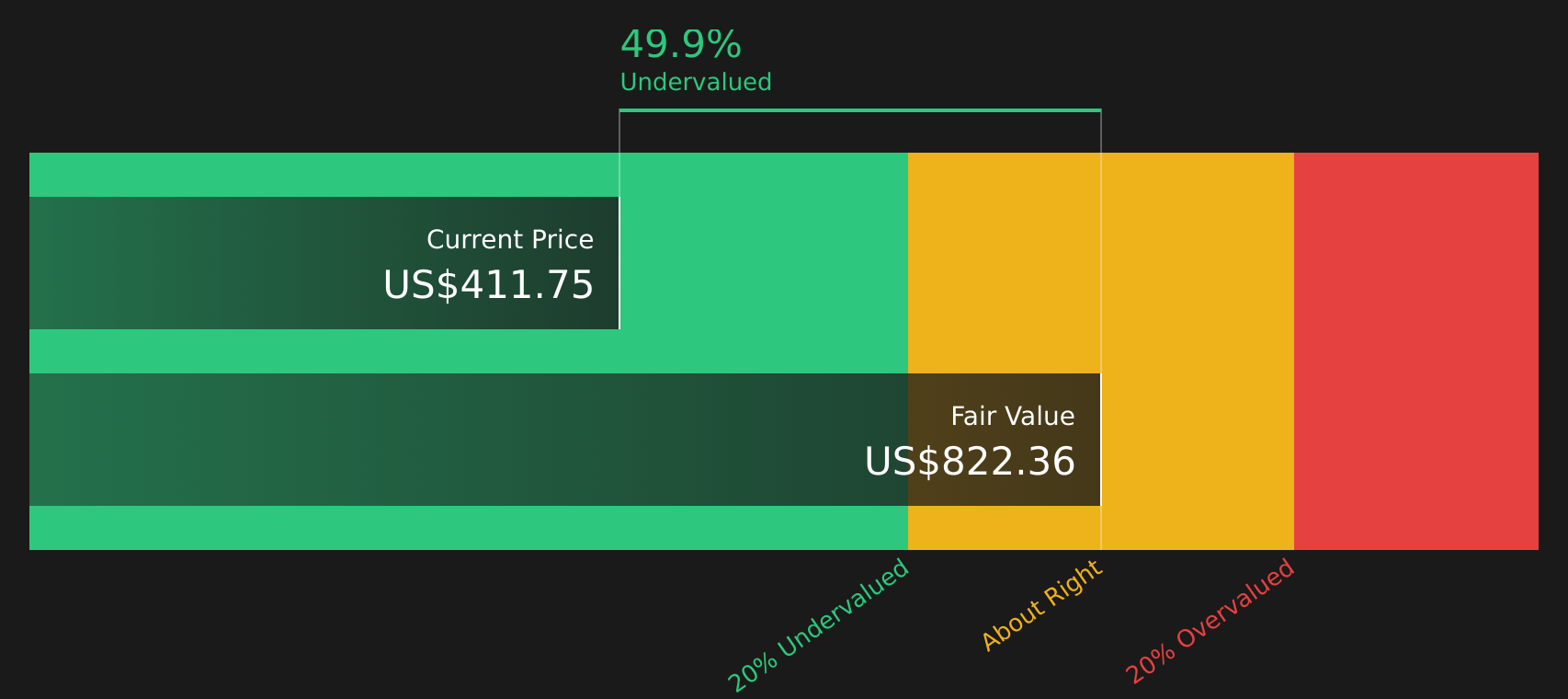

A Discounted Cash Flow, or DCF, model estimates what a company could be worth by projecting its future cash flows and discounting them back to today using a required rate of return. It is essentially asking what those future dollars are worth in current terms.

For FedEx, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections. The latest twelve month free cash flow is about $3.6b. Analyst inputs and extrapolations then build a path where projected free cash flow reaches $8.3b by 2029, and continues through to 2035 with estimates ranging from about $4.5b to $14.2b over that 10 year span, all expressed in discounted form to reflect time value and risk.

Bringing all those projected cash flows back to today results in an estimated intrinsic value of $763.68 per share, compared with the current share price of $355.78. On this model, the stock screens as about 53.4% undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests FedEx is undervalued by 53.4%. Track this in your watchlist or portfolio, or discover 55 more high quality undervalued stocks.

Approach 2: FedEx Price vs Earnings

For a company that is generating profits, the P/E ratio is a straightforward way to see how much investors are paying for each dollar of earnings. It helps you quickly compare what the market is willing to pay for one business versus another that is also profitable.

What counts as a "normal" P/E depends on how the market views a company’s growth potential and risk. Higher expected growth and lower perceived risk often line up with a higher P/E, while lower growth expectations or higher risk usually go with a lower P/E.

FedEx currently trades on a P/E of 18.96x. That is above the Logistics industry average of 15.06x, but below the peer group average of 21.55x. Simply Wall St’s Fair Ratio for FedEx is 23.80x, which is a proprietary estimate of what the P/E could be given factors such as earnings growth characteristics, profit margins, size, industry and company specific risks. This Fair Ratio can be more informative than a simple industry or peer comparison because it adjusts for these business specific features rather than assuming all companies deserve similar multiples. On this lens, FedEx’s current P/E is below the Fair Ratio, which indicates that the shares screen as undervalued on an earnings multiple basis.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your FedEx Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as your way of attaching a clear story about FedEx to the numbers you see, including your own view of fair value and estimates for future revenue, earnings and margins.

A Narrative on Simply Wall St connects three things: the business story you believe, the financial forecast that story implies, and the fair value that drops out of those assumptions, all in one place on the Community page that millions of investors use.

Once you have a FedEx Narrative, the platform compares your Fair Value to the current share price to help you decide whether the stock looks expensive or cheap relative to your own story. It then keeps that view current by updating the Narrative when new information such as earnings, guidance or news is added.

For example, one FedEx Narrative might lean closer to the higher fair value estimates around US$384.96 or US$371.45 that focus on cost efficiencies and Network 2.0. Another might sit nearer the lower fair value of about US$233.77 that leans more heavily on freight risks and more cautious revenue assumptions, and both can coexist side by side so you can see exactly which story you agree with.

For FedEx, however, we will make it really easy for you with previews of two leading FedEx Narratives:

Fair value: US$384.96

Discount to fair value: 7.6% based on the current share price of US$355.78

Revenue growth assumption: 4.56% a year

- Focuses on DRIVE cost savings, Network 2.0 and Tricolor efficiency gains to support margins and earnings.

- Builds in moderate revenue growth, a modest uplift in profit margins and regular share buybacks to support earnings per share.

- Uses an analyst consensus fair value that sits below the DCF output but above more cautious scenarios, with a P/E that remains below the wider US Logistics industry level cited in the narrative.

Fair value: US$233.77

Premium to fair value: 52.1% based on the current share price of US$355.78

Revenue growth assumption: 2.04% a year

- Emphasises structural headwinds such as potential parcel volume pressure, higher environmental and labor costs and tougher competition from e commerce platforms and regional carriers.

- Assumes more cautious revenue growth and margins, along with a lower future P/E multiple to reflect freight uncertainty and execution risk.

- Highlights the risk that current expectations and valuation could be ahead of what more conservative earnings and freight assumptions would support.

Do you think there's more to the story for FedEx? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com